Ever wondered how global banking stays (relatively) stable? The answer lies, in large part, with a series of international agreements, the first of which is Basel I a foundational accord that shaped modern banking regulations. Born from the collective wisdom of central bankers navigating the turbulent financial waters of the late 1970s and 1980s, Basel I marked the beginning of a concerted effort to harmonize banking standards across borders.

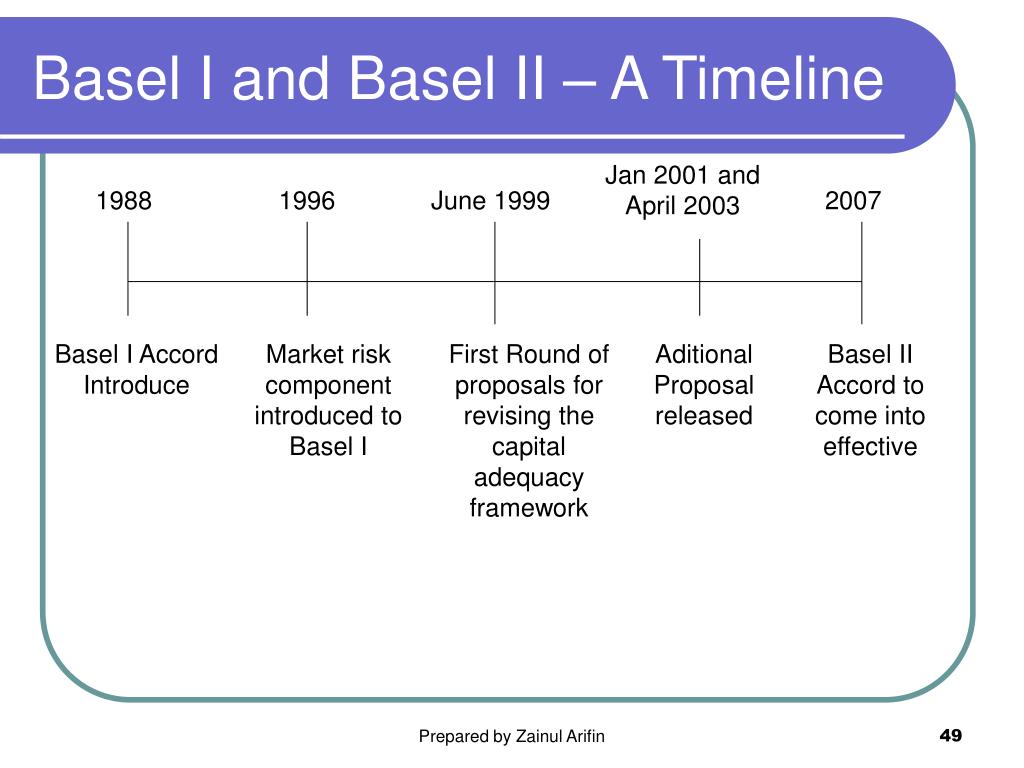

The journey began in Basel, Switzerland, at the Basel Committee on Banking Supervision (BCBS). In 1988, this committee, comprised of representatives from major economies, published its initial set of minimum capital requirements for banks. This wasn't just a suggestion; it was a benchmark intended to be implemented by member jurisdictions, impacting internationally active banks worldwide. The core of Basel I revolved around managing capital risk, market risk, and operational risk the trifecta of concerns that could destabilize financial institutions. Understanding Basel I requires delving into its key features and appreciating its impact on the global banking landscape.

| Category | Details |

|---|---|

| Name | Basel I (Basel Capital Accord) |

| Year Established | 1988 |

| Originating Body | Basel Committee on Banking Supervision (BCBS) |

| Location of BCBS | Basel, Switzerland |

| Purpose | Establish minimum capital requirements for banks to mitigate credit risk. |

| Key Focus | Credit Risk |

| Risk Weight Categories | Assets divided into four categories with varying risk weights (0%, 20%, 50%, 100%) |

| Implementation | Implemented by member countries of the BCBS. |

| Amendments | Amended in 1998 to include provisions for loan losses. |

| Predecessor | None (First international regulatory framework for banks) |

| Successors | Basel II, Basel III |

| Impact | Standardized capital adequacy measurement across countries. |

| Limitations | Simplistic approach to risk assessment; primarily focused on credit risk. |

| Legacy | Laid the foundation for subsequent Basel Accords and international banking regulations. |

| Reference Link | BIS Website (Basel Committee on Banking Supervision) |

One of the defining aspects of Basel I was its global reach. The framework extended beyond the BCBS member countries, influencing banking practices worldwide. This broad adoption stemmed from the need for a unified approach to managing financial risk in an increasingly interconnected world. The accord also evolved over time, with a notable amendment in 1998 addressing general provisions for loan losses. This demonstrated a willingness to adapt the framework to address emerging challenges and refine its effectiveness.

- Meet Eloise Schwarzenegger Pratt The Rising Star Of Hollywood

- Meet The Mysterious And Charismatic Cillian Murphy As Batman Beyond The Cape And Cowl

The initial Basel I accord primarily focused on credit risks and monetary risks, recognizing these as the most pressing threats to the stability of banking institutions. It defined operations risks in a negative way. This initial focus shaped the structure of the framework, leading to specific requirements and guidelines designed to mitigate these particular risks.

Looking back, the evolution from Basel I to the current regulatory landscape highlights the continuous adaptation required to keep pace with a dynamic financial environment. What started as a relatively simple framework has expanded and become more complex to address new challenges and incorporate lessons learned from past crises.

Navigating the Basel framework today involves considering regional variations, analyzing case studies, integrating sustainability considerations, conducting stress testing, understanding the impact on SMEs (small and medium-sized enterprises), and adapting to fintech innovations. This multifaceted approach underscores the ongoing evolution of global banking regulations.

- Has Cris Collinsworth Hung Up His Broadcasting Hat

- The Quintessential Sitcom Dad Dan Conner From Roseanne

Analysis conducted by firms like KPMG further underscored the need for evolution. Their assessments revealed that a comprehensive overhaul of the Basel II protocols was necessary to address shortcomings and ensure the continued stability of the financial system. This ultimately led to the development of Basel III, a further refinement of international banking regulations.

The term "Basel I" is commonly used to refer to the 1988 Basel Capital Accord. This accord represented a significant step forward in establishing international capital requirements for banks, setting a precedent for future regulatory efforts. The BCBS framework itself is a comprehensive set of standards that serves as the primary global standard setter for the prudential regulation of banks. These standards are designed to ensure that banks operate in a safe and sound manner, protecting depositors and the financial system as a whole.

Basel I norms, established in 1988, were the first accepted framework aimed at addressing the capital adequacy issue within the banking sector. It was the inaugural global regulatory framework introduced by the BCBS to tackle this critical challenge.

As the first accord issued by the BCBS in 1988, Basel I established a foundation for subsequent regulations. It divided bank assets into four broad risk categories, assigning different risk weights to each. This categorization allowed for a more standardized approach to assessing and managing risk across different banking institutions.

It's important to note that, in Basel I, the Basel Committee approached the definition of operations risks negatively. They proposed revisions in subsequent accords to provide a more comprehensive and positive definition of these risks.

Basel II emerged as a response to the limitations of Basel I, aiming to refine regulations and improve overall regulatory effectiveness. Basel III, in turn, built upon Basel II, further enhancing banking regulations based on the lessons learned and the evolving financial landscape.

So, how did Basel I affect banks? The accord had a profound impact on how banks managed their capital and assessed risk. It forced them to adopt more rigorous standards and to hold more capital in reserve to protect against potential losses.

The Federal Reserve Board of Governors in Washington D.C., plays a crucial role in implementing and enforcing these international regulatory capital standards within the United States. The US actively participates in the BCBS, contributing to the development of these standards through various capital accords and related publications that have been in effect since 1988.

The severe financial crisis of 2008-2009 exposed vulnerabilities in the existing regulatory framework. In response, the Basel Committee established stricter financial regulations and guidelines, leading to the development of Basel III. These regulations are often referred to collectively as Basel I, Basel II, and Basel III, representing the evolution of international banking standards.

The BCBS instigated the Basel I accord in 1988 as a direct response to the liquidation of a bank that highlighted the need for stronger capital requirements. This event served as a catalyst for the development of the international framework.

The Basel I accord was the result of extensive consultations and deliberations among central bankers from around the world. This collaborative effort culminated in the publication of a set of minimum capital requirements for banks, marking a significant milestone in international banking regulation.

Basel III (2010) was developed in response to the 2008 global financial crisis, which revealed significant gaps in the Basel II framework. Basel III expanded the framework, focusing on improving banks' resilience during periods of economic distress. It introduced stricter capital requirements, new liquidity standards, and measures to mitigate systemic risk.

To truly grasp the significance of Basel I, consider its fundamental principles. The accord aimed to create a level playing field for international banks by establishing consistent capital adequacy requirements. This meant that banks operating in different countries would be subject to similar rules, reducing the potential for regulatory arbitrage and promoting fair competition.

Furthermore, Basel I sought to improve the overall stability of the financial system. By requiring banks to hold more capital, the accord aimed to make them more resilient to economic shocks and less likely to fail. This, in turn, would protect depositors and prevent the spread of financial contagion.

The framework operated by assigning risk weights to different types of assets held by banks. Assets considered to be riskier, such as loans to borrowers with poor credit histories, were assigned higher risk weights. This meant that banks were required to hold more capital against these assets.

The risk weights were based on a relatively simple categorization of assets. The four broad risk categories were: 0%, 20%, 50%, and 100%. Government bonds, for example, were typically assigned a 0% risk weight, while loans to private sector companies were assigned a 100% risk weight.

While Basel I represented a significant step forward, it also had its limitations. One of the main criticisms was its simplistic approach to risk assessment. The framework relied on broad categories and did not adequately differentiate between different levels of risk within those categories.

For example, all loans to private sector companies were assigned a 100% risk weight, regardless of the creditworthiness of the borrower. This could lead to banks being penalized for lending to creditworthy companies, while not being adequately incentivized to avoid lending to riskier companies.

Another limitation of Basel I was its focus primarily on credit risk. While credit risk is certainly a major concern for banks, it is not the only type of risk they face. Market risk, operational risk, and liquidity risk can also pose significant threats to financial stability.

Despite its limitations, Basel I laid the foundation for subsequent Basel Accords, including Basel II and Basel III. These later accords addressed many of the shortcomings of Basel I and introduced more sophisticated approaches to risk management.

Basel II, for example, introduced a three-pillar approach to regulation. Pillar 1 focused on minimum capital requirements, Pillar 2 focused on supervisory review, and Pillar 3 focused on market discipline. This broader approach to regulation aimed to address a wider range of risks and to promote greater transparency in the banking sector.

Basel III, in turn, built upon Basel II by introducing stricter capital requirements, new liquidity standards, and measures to mitigate systemic risk. These measures were designed to make banks more resilient to economic shocks and to prevent future financial crises.

The journey from Basel I to Basel III reflects the ongoing effort to improve the regulation of the global banking system. While no regulatory framework is perfect, the Basel Accords have played a significant role in promoting financial stability and protecting depositors.

The impact of Basel I extended beyond the banking sector. The accord also influenced the development of risk management practices in other industries, such as insurance and investment management.

Companies in these industries began to adopt similar approaches to risk assessment and capital management, recognizing the importance of these practices for their own financial stability.

Furthermore, Basel I helped to promote greater transparency in the financial system. By requiring banks to disclose information about their capital adequacy and risk management practices, the accord made it easier for investors and regulators to assess the health of the banking sector.

This increased transparency helped to build confidence in the financial system and to reduce the potential for financial crises.

In conclusion, Basel I was a landmark agreement that had a profound impact on the global banking system. While it had its limitations, it laid the foundation for subsequent regulatory efforts and helped to promote greater financial stability. Its legacy continues to shape the way banks manage risk and capital today.

Looking ahead, the Basel framework will continue to evolve in response to new challenges and opportunities. The rise of fintech, for example, is creating new risks and opportunities for the banking sector, and regulators will need to adapt their approaches to address these developments.

Sustainability is another area that is likely to play an increasingly important role in the Basel framework. Banks are increasingly being asked to consider the environmental and social impact of their lending decisions, and regulators may need to incorporate these considerations into their capital requirements.

The Basel Committee on Banking Supervision (BCBS) remains committed to promoting financial stability and protecting depositors. The committee will continue to work with its member countries to refine the Basel framework and to ensure that it remains relevant in a rapidly changing world.

The ongoing evolution of the Basel framework is a testament to the importance of international cooperation in addressing global financial challenges. By working together, countries can create a more stable and resilient financial system that benefits everyone.

Basel I, therefore, stands as a crucial first step in a long and ongoing journey toward a more secure and stable global financial system.

The initial impact of Basel I on individual banks manifested in several key areas. First, it required banks to enhance their internal risk management systems. Before Basel I, many banks relied on relatively unsophisticated methods for assessing and managing risk. The new accord compelled them to adopt more rigorous and standardized approaches, leading to significant investments in technology and personnel training.

Second, Basel I spurred a wave of innovation in financial products. Banks sought to optimize their capital allocation by developing new financial instruments that could reduce their risk-weighted assets. This led to the growth of securitization, derivatives, and other complex financial products, some of which later contributed to the 2008 financial crisis. This highlights the double-edged sword of regulatory innovation: while it can improve capital efficiency, it can also create new and unforeseen risks.

Third, Basel I influenced the geographical distribution of banking activity. Banks in countries with stricter regulatory enforcement faced a competitive disadvantage compared to those in countries with laxer enforcement. This created incentives for banks to shift their operations to jurisdictions with more favorable regulatory environments, a phenomenon known as regulatory arbitrage. This underscores the importance of consistent and coordinated implementation of international regulations across all jurisdictions.

The long-term consequences of Basel I extended far beyond the immediate impact on individual banks. The accord played a crucial role in shaping the global financial landscape, fostering greater integration and interdependence among national banking systems.

However, it also contributed to the build-up of systemic risk. By encouraging banks to take on more complex and opaque financial instruments, Basel I inadvertently increased the interconnectedness of the financial system, making it more vulnerable to shocks.

The 2008 financial crisis exposed the limitations of Basel I and its successor, Basel II. The crisis revealed that the existing regulatory framework was inadequate to address the risks posed by complex financial products and the interconnectedness of the global financial system.

The crisis led to a fundamental rethinking of banking regulation, culminating in the development of Basel III. Basel III introduced a range of reforms designed to strengthen bank capital, improve liquidity, and reduce systemic risk. These reforms represent a significant step forward in the regulation of the global banking system.

Despite the progress made with Basel III, challenges remain. One of the main challenges is ensuring consistent and coordinated implementation of the regulations across all jurisdictions. Regulatory arbitrage remains a significant concern, as banks continue to seek out jurisdictions with more favorable regulatory environments.

Another challenge is adapting the regulatory framework to keep pace with the rapid pace of innovation in the financial industry. New technologies, such as blockchain and artificial intelligence, are creating new opportunities and risks for the banking sector, and regulators will need to be nimble and adaptable in order to address these developments.

The evolution of the Basel Accords is a continuous process. As the financial landscape changes, so too must the regulatory framework. The Basel Committee on Banking Supervision (BCBS) remains committed to promoting financial stability and protecting depositors, and it will continue to work with its member countries to refine the Basel framework and to ensure that it remains relevant in a rapidly changing world.

In conclusion, Basel I was a groundbreaking agreement that laid the foundation for modern banking regulation. While it had its limitations, it played a crucial role in promoting financial stability and protecting depositors. Its legacy continues to shape the way banks manage risk and capital today, and its influence will continue to be felt for years to come.

- Breaking News Boris Sanchez Joins Cnn As Senior Correspondent

- How Old Is Eminem Find Out The Rappers Age

:max_bytes(150000):strip_icc()/BaselIIAccordGuardsAgainstFinancialShocks1-fb23a015d23643009e189c8f43c74a03.png)